Bumpy Road for the Bulls Lies Ahead

Fifty-five days into the first quarter of 2020, I want to offer a few observations about stocks, bond yields, currencies, gold, debt and politics.

I want to assess whether any single factor or combination may pose a risk to the bull trend that has the S&P on a trajectory to trade to 3,500 a lot sooner than the majority of market pros are predicting. I’ll just list them off and summarize:

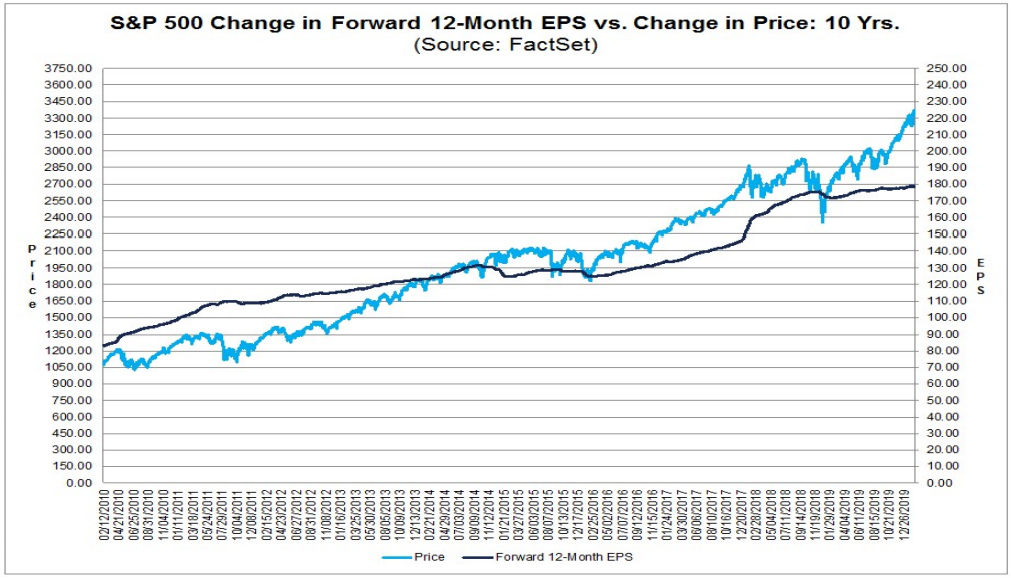

- According to FactSet, as of Feb. 14, the forward 12-month price-to-earnings (P/E) ratio for the S&P 500 is 18.9. This P/E ratio is above the five-year average, 16.7, and above the 10-year average, 15.0. Earnings are forecast to be 2% in the first quarter and rise to 5% growth in the second quarter. The market is betting that forward earnings growth will narrow the P/E premium.

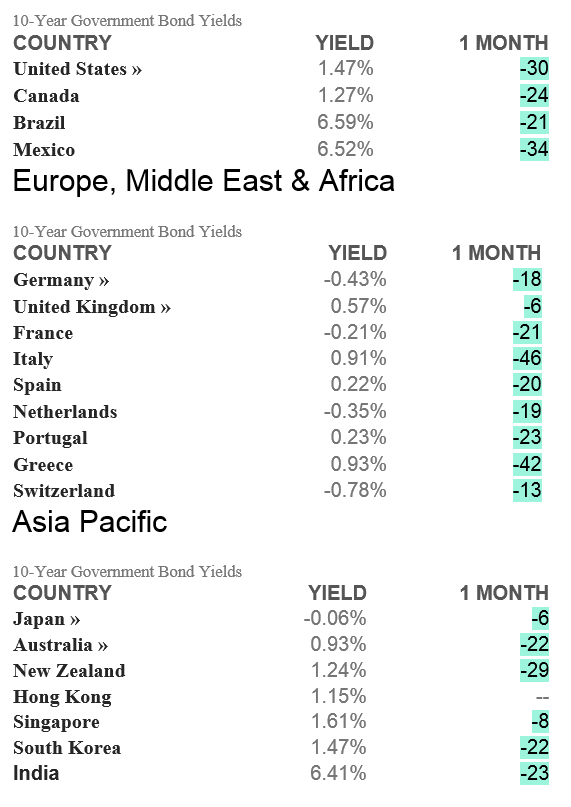

- Sovereign bond yields are in sharp decline again around the globe. This is a rather sudden development where the U.S. 2/10 year spread briefly inverted two weeks ago. This kind of price movement would portend that more quantitative easing (QE) and future cuts in overnight lending rates are in store to sustain a nascent global recovery.10-Year Government Bond Yields; one-month rate of change (in basis points)

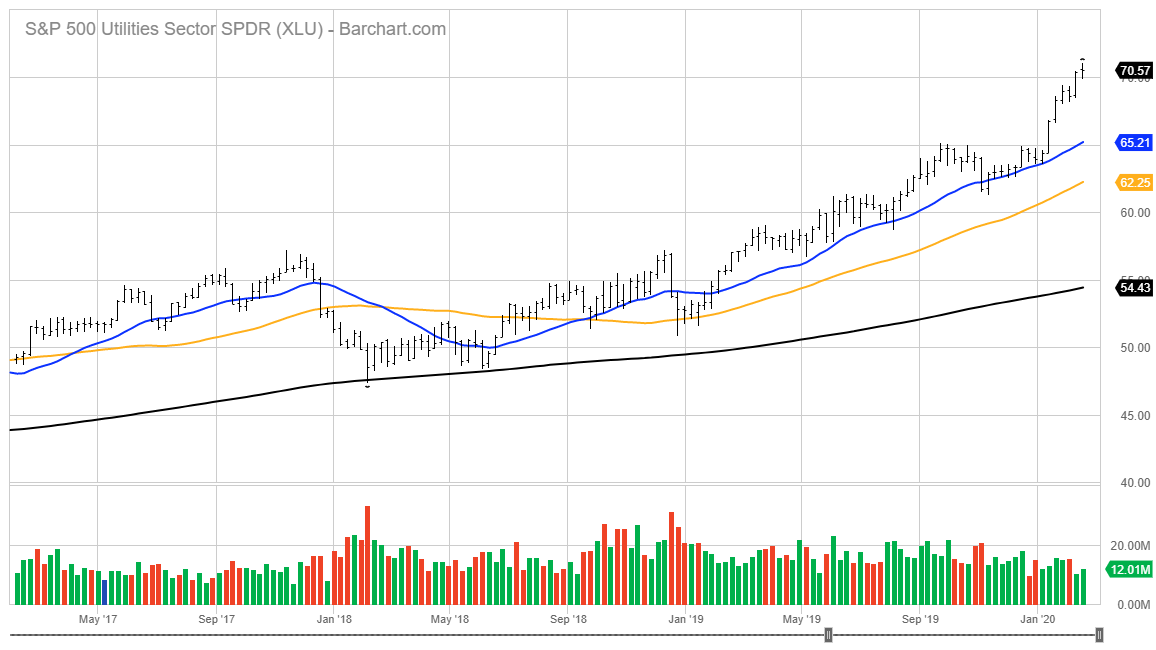

- The safe haven sectors are not giving way to the supposed risk-on trade in equities. There is no natural rotation from risk adverse stocks taking place. The consumer staples, utility and real estate investment trust (REIT) sectors are trading at new all-time highs.

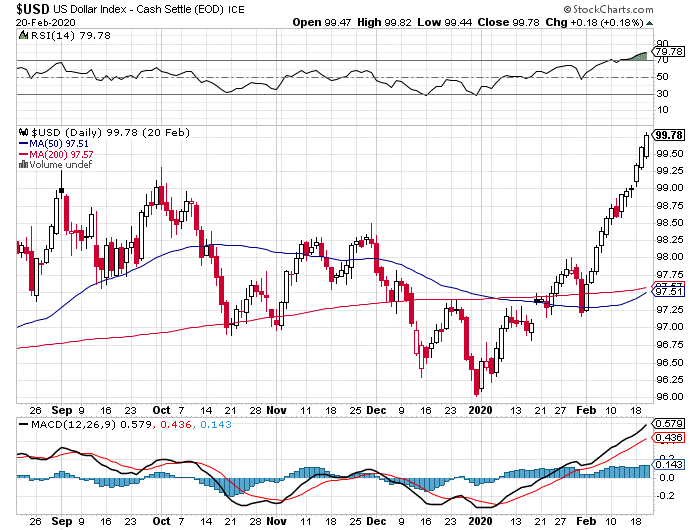

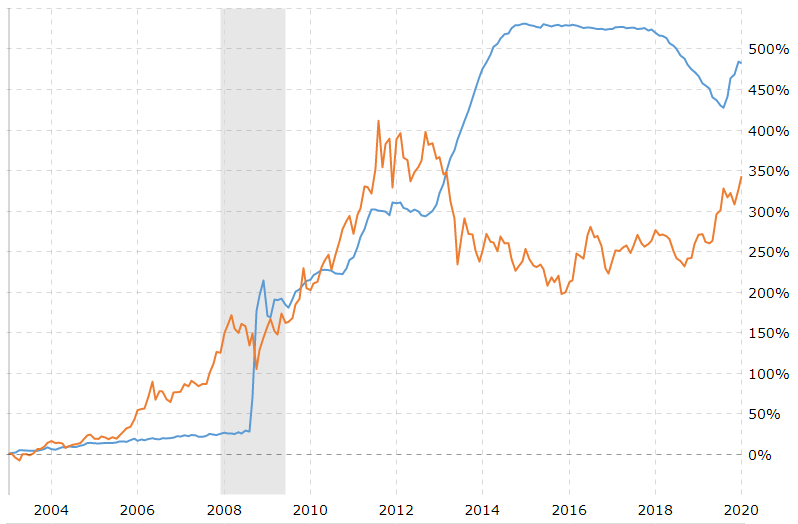

- The dollar is surging against all other currencies since the Fed is expanding its balance sheet. It currently is at $4.2 trillion and near the 2015 QE high of $4.5 trillion. This is a counterintuitive development and will be an earnings headwind in the first quarter if the rally in the greenback continues.

- Gold prices are looking like they may revisit the September 11, 2011, high of $1,895 per troy ounce. At the current price of $1,645/oz., the United States is the largest holder of gold in the world with 8,133 tonnes of gold bullion. Central banks have been the biggest buyers of gold since 2010 as a hedge against devaluation of currencies.

Fed Balance Sheet (blue line) – Price of Gold (green line)

Source: Macrotrends

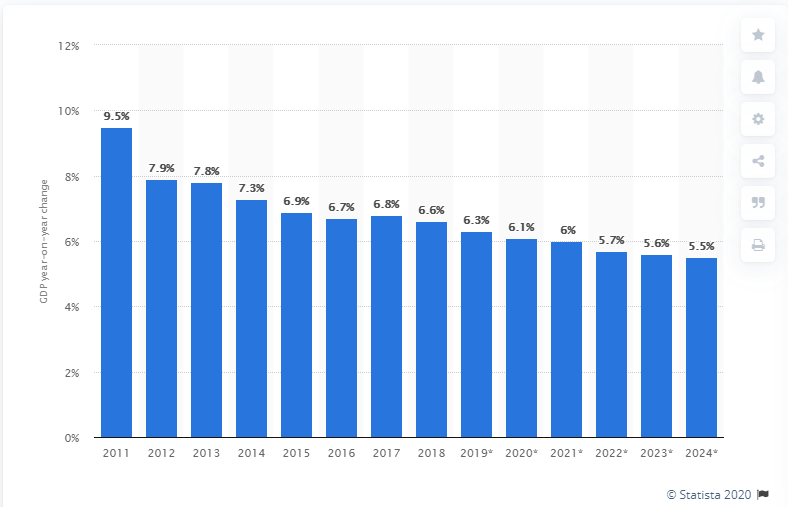

- China’s growth rate of gross domestic product (GDP) is sure to slide under 6% this year from the impact of coronavirus. Add to that fresh situation allegations of spying by Huawei. Just last month, the Justice Department announced charges against Huawei, including fraud, theft and obstruction of justice as it pertains to intellectual property and privacy. I would venture to say that any notion of a Phase two deal is formally on ice.

This is quite a collage of inputs for the stock market to absorb and digest. There’s a lot of moving parts and all these factors are fluid for sure. Most of the six issues noted above would be considered yellow caution flags for the current rally, at least from a historical perspective. And yet for reasons beyond what most market professionals can explain, the U.S. stock market and most of those around the world are pushing higher.

The coast seems clear for the S&P to trade to 3,500 and beyond following the current coronavirus-related pullback. That view holds amid rising optimism about the secular outlook for the global economy, the shrinking size of the U.S. and other stock markets relative to the ocean of liquidity with more QE to come, or the idea that a spike in inflationary or deflationary pressures won’t emerge anytime soon.

There will be some speed bumps for sure. Count on it. We live in a world of high-powered tweets and algorithm-driven trading platforms that rule the tape every day. But as long as jobs are plentiful and the costs to operate businesses and manage households are reasonable, then these are the more powerful overriding forces that are dominating the investing landscape. At least that is this man’s view of the crazy world in which we live. Money still goes where it is best served — the U.S. stock market.