Big Signs of Trouble Facing Italian Debt Market

As the bull market for U.S. stocks continues to grind higher, much is being made of the trade war with China, the threat of U.S. defection from the World Trade Organization (WTO) and sanctions against Russia and Iran.

Individually, these issues are important, but they are not rally killers. However, one issue that might be a game changer in the months ahead is the ultimate fate of deteriorating creditworthiness of public debt and souring emerging market debt held by developed banks — namely those in Italy.

Bond vigilantes, a term for investors who sell the bonds of governments when they run big deficits and appear to have unsustainable debt burdens, and short sellers of Italian bank stocks are starting to reap the profits of placing big bets earlier this year.

According to data from Italy’s financial regulator Consob, Bridgewater, the world’s largest hedge fund, has a number of short positions on Italian financial institutions, including UniCredit, Italy’s biggest bank. Other funds betting against Italian companies include Steven Cohen’s Point72 Asset Management, London-based Marshall Wace and quantitative specialist AQR Capital Management.

Adverse headlines and fears of downgrades are both likely to remain factors ahead of the European Commission’s review of Italy’s budget plans, with credit-rating firm Moody’s set to complete a review by the end of October, said Giovanni Montatti, analyst at UBS, in a note. Italy is rated Baa2 by Moody’s, two notches above junk.

European markets are starting to consider how short Italy’s public debt maturity is and how exposed the country is to the whims of the global bond market. Italy’s public debt is officially estimated to be at around 133% of gross domestic product (GDP), making Italy the second-most-indebted country in the euro zone after Greece. However, the official Italian debt numbers do not include the Bank of Italy’s debtor position of more than EUR400 billion in the European Central Bank’s Target2 accounts.

TARGET2 is the real-time gross settlement system owned and operated by the Eurosystem, the monetary authority of the euro zone. TARGET stands for Trans-European Automated Real-time Gross settlement Express Transfer system, and TARGET2 denotes the second generation. It is a Single Shared Platform (SSP) operated by three central banks: France (Banque de France), Germany (Deutsche Bundesbank) and Italy (Banca d’Italia). In short, TARGET2 is a massive clearing system which balances out cross-border financial movements with the euro zone.

If one adds the Bank of Italy’s Target2 liabilities to the Italian public debt total, the public debt to GDP ratio rises to 160%, taking that ratio to its highest level in over 100 years. Italian bank shares came under intense pressure last Friday as prices for the country’s sovereign debt dropped sharply, putting the sector in investors’ crosshairs. Shares in the country’s major banks fell, with Italy’s largest bank, UniCredit S.p.A., sliding more than 6.7% in a day after the country’s populist government agreed to a budget with bigger spending plans than expected. The move puts the bank’s stock near the 52-week low with decidedly negative money flows right now.

Source: BigCharts.com

The new Italian government’s budget-busting proposal is about to make the country’s public debt market even more unsustainable. Some of the factors involved include the introduction of a guaranteed basic income and flat income tax. When combined, they increase Italy’s budget deficit by $100 billion euros.

An argument could be made that Italian Prime Minister Giuseppe Conte is taking a page out of the Trump playbook — using debt as a weapon for future growth. However, Italy is not America, and trying such a strategy in the face of potentially exploding entitlement costs was not what the market wanted to see unfold. As a result, the Italian stock markets tanked.

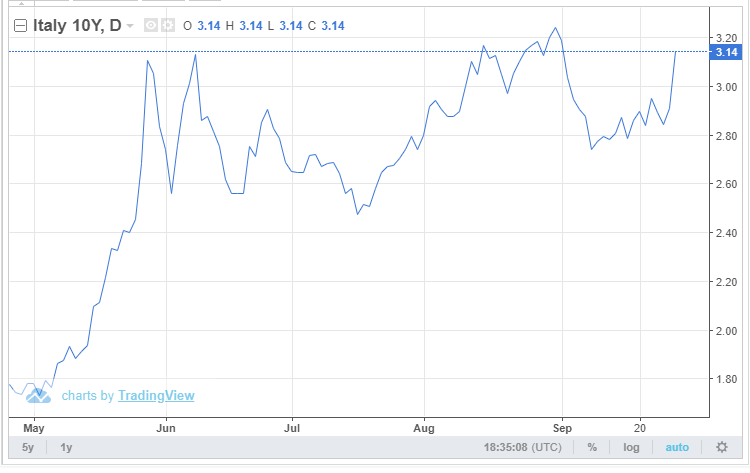

Tale of Two 10-Year Yields

The yield on the 10-year benchmark Italian bond jumped 24 basis points to hit 3.15% and has been volatile since the League and Five Star parties formed a coalition government in early June, promising to boost public spending, cut taxes and reverse unpopular pension reforms. This kind of political agenda is akin to someone saying, “I’m going to the mall to shop for Christmas presents,” after just being laid off from work. While the U.S. 10-year Treasury note currently trades around the same 3.1% yield, it does so through its relationship to a strengthening and vibrant economy. For Italy, the spike in the 10-year yield in the past four months is due to deteriorating economic fundamentals and balance sheet risk.

Why this sudden turn of events matters, when most other global events have been brushed off by the U.S. stock market, is that Italy’s economy is significant to the well-being of the rest of the world. As the third-largest economy in the euro zone and the eighth-largest by nominal GDP in the world, a financial crisis in Italy carries with it real potential for contagion.

The Italian economy might rank eighth in the world, but the Italian bond market is the third-largest ($2.5 trillion) in the world behind the United States and China. While the prevailing view is that the European Central Bank (ECB) will sweep like a cavalry charge if the blood-letting starts in the Italian bond market, there could be negative implications beyond the country’s borders.

If the Italian government does not become more fiscally responsible soon, investors should brace for another European sovereign debt crisis. Italian banks’ non-performing loans amount to as much as 15% of their balance sheets, while an additional 10% of the balance sheets are made up of Italian public debt bonds. It should be no wonder then why hedge funds are holding a double-barreled short position in both Italian bonds and Italian bank stocks. The trades are working like a champ.

It will be interesting to see how this highly fluid scenario plays out over the next few weeks and months. However, it is safe to say it’s not where I would recommend investors seek yield in global markets. By comparison, U.S. investment-grade corporate bonds can be found that are currently paying over 4% with an average maturity of 7-10 years. There is no reason, in my view, to venture out of the U.S. bond market for competing yield.

By all means, travel to Italy and take full advantage of how far the strong dollar will stretch, but leave your investing capital at home in the United States. There are excellent high-yield opportunities within our domestic market, and I highlight some of my favorite picks in my Cash Machine advisory service. Within this service, I have crafted a portfolio of about 22 holdings from various asset classes that pays a blended yield of 8.4%.

I combine real estate investment trusts (REITs), master limited partnerships (MLPs), business development companies (BDCs), closed-end funds and common stocks to generate a fantastic overall yield with the dual mandate of producing long-term capital gains, as well. If high-performance income is a goal, then look no further than Cash Machine. Thousands of investors already have put my high-yield portfolio to work, and 2018 is shaping up to be another banner year for the model portfolio.