Year-End Forecast Has Stocks Up and Bond Yields Down

Approaching the midpoint of the month with only 14 trading days left in 2017, we’re seeing the first signs of a Santa Claus rally triggered by a very robust employment report.

Non-Farm Payrolls added 228,000 jobs versus consensus of 190,000 with the Unemployment Rate staying at 4.1%. The November Employment Situation report was basically more of the same with respect to labor market activity.

Job growth was strong, but wage growth wasn’t. The key takeaway from the report is that wage growth remains subdued. That isn’t likely to keep the Fed from raising rates at this month’s meeting, yet it could give the Fed a data-based reason to move more slowly on the next rate hike in 2018.

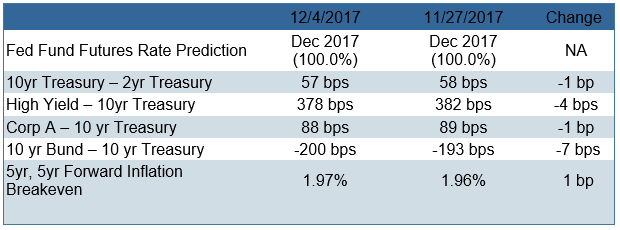

This past week, the Treasury market saw a continuation of the yield curve flattening trend, though the 2s10s spread, which identifies the difference in yield between the 2-year Treasury Note and the 10-year Treasury Note, dipped just one basis point to 57 bps. While last week’s contraction was minor, it is worth remembering that the 2s10s spread has contracted 72 basis points over the past year, leading to an uptick in worries about a slowdown in economic growth. Broadly speaking, the market’s focus during the past week was on the progress of the Senate tax bill, which will now head to a conference committee, where differences between the Senate and House versions will be reconciled.

The yield spread between Germany’s 10-year bund and the U.S. Treasury 10-year note contracted seven basis points to -200 after a five-basis-point expansion took place one week ago. Inflation expectations expressed by the 5-year, 5-year forward rate, which is a measure of expected inflation (on average) over the five-year period that begins five years from today, saw another very slight uptick, rising one basis point to 1.97% to stay below the 2.00% level. The fed funds futures market remains certain that the Federal Open Market Committee (FOMC) will call for a 25-bps rate hike at the December meeting. Looking past December, the fed funds futures market shows a 61.4% implied likelihood of another rate hike in March.

I and others on this post have been spending time these past couple of weeks on the topic of the flattening yield curve and whether it portends to trouble ahead as in past economic cycles. I remain camped out in the view that the current lid on wage inflation, coupled with strong economic and earnings data, will feed investor optimism further and push stocks higher. I can’t remember a time within my 33 years as an investment professional where this set of conditions existed. Typically, at this juncture of low unemployment and gross domestic product (GDP) running above 3%, upward pressure on wages would be not just a given, but widely evident in the jobs data.

For now, though, it just isn’t there and without question is the biggest headwind to a bull market. This is because it brings with it the highly unwelcome uncertainty of how high the inflation rate could go, which, in turn, causes the Fed to hike rates faster than expected. The fact that the inflation genie is still being kept in the bottle gives the stock market a green light to trade meaningfully higher with or without tax reform. And we’ll know more about what the final tax package looks like later this week when the Senate and House versions go to conference for reconciliation towards a final bill. The elimination of the state income tax deduction is a major sticking point that easily could threaten passage by the end of the year.

Next Stop for S&P Is a Big Round Number

However, investors are quite sure about a final version becoming law, followed by a smooth transition from outgoing Fed Chair Janet Yellen to her successor Jerome Powell on Feb. 3. As a result, the sky for the bullish stock camp is bright blue. The S&P has just broken out once again at 2,600 and is technically well on its way to 3,000 by this time next year — barring a black swan event. That’s a 13.2% move up for the S&P and one that is very achievable given the current economic outlook.

For the moment, I think I might be on my own island calling for a target of 3,000 for the S&P. But once fourth-quarter earnings season gets under way and it becomes clear how the macro data feeds into strong quarterly earnings results, I doubt that I will be alone or among the few. Not only is inflation a non-threat now, the futures market doesn’t see it as much of a threat five years out. Under these circumstances, the flat yield curve should be viewed as ironically bullish in that history might show it to have been a leading indicator of a prolonged economic expansion and not a warning flag that precedes a recession.

Financial engineering (six years of quantitative easing) revived the patient (domestic economy) and only recently has the patient started to breath on its own. The Fed refrained from paring its bloated $4.5 trillion balance sheet until it was sure the economy was good and ready. As of this October, that process has begun with the Fed letting maturing Bonds “roll off” its portfolio rather than selling Treasuries outright. This process could take five to seven years, according to former Fed Chairman Ben Bernanke, and it would help greatly to minimize another “taper tantrum” in the stock market. This blueprint for unwinding quantitative easing is seen by market participants as prudent and is why the bull market has a lot of snort left in it.

In case you missed it, I encourage you to read my e-letter from last week about how tax reform can add more fuel to the stock market.