Offsetting Currents Leave Market in Flux as Bond Yields Rise

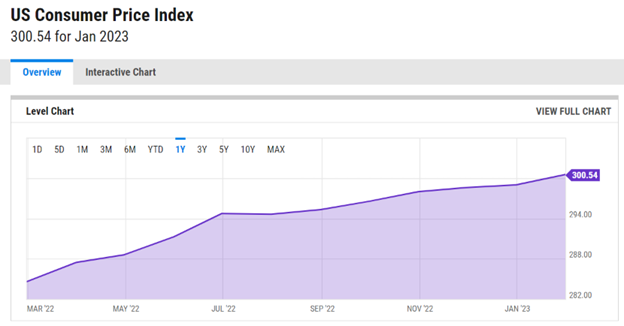

The investing landscape is about as mixed and garbled as one could imagine, with all the conflicting data showing a lot of fragmentation within several sectors of the economy amid tightening monetary policy, and a stock market that is demonstrating resilience against seemingly mounting odds. The bears point to an inverted yield curve, a hot shelter index within the CPI, lower oil prices, negative monthly manufacturing data, flat growth in industrial production, talk of a 50-basis-point (BPS) hike at the March 22 FOMC meeting, record household credit and a resumption of rising commodity prices.

Source: www.ycharts.com

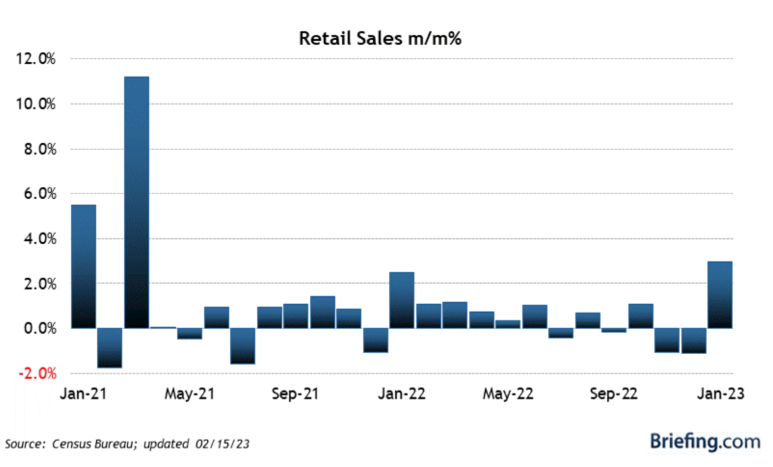

It is widely understood that the consumer drives U.S. GDP, and though anecdotal evidence would suggest the consumer is just fine, the hard data would imply otherwise, to be sure. Consumer spending was nothing short of spectacular in January, buttressing everything from new car purchases, travel, hospitality, entertainment, furniture, home furnishings, electronics, clothing and accessories. The key takeaway from the report is that consumers were spending freely on goods in January, despite the ongoing inflation pressure. In fact, every single sales category showed a month-over-month increase, led by a 7.2% surge in sales at food-and-beverage establishments.

The narrative that has been making the rounds within investment circles to explain this “damn inflation, full spending ahead” is a strange and surreal admission by believers of LTS — i.e., life’s too short. Others in the financial world would call this whistling by the graveyard, and that all the stimulus and relief experienced during the pandemic infected millions upon millions of people with the idea that extreme debt is no big deal.

After all, the federal government has no problem running up $31.46 trillion in debt and mortgaging the future of our great-grandchildren. It’s like, “when my stuff hits the fan, I’ll just stop paying on my rent, cry foul when they come to repossess my Tesla, wait for the government to bail me out of my student loans and go tell my credit card issuers to go pound sand, because you shouldn’t have extended me that much credit in the first place. It’s not my fault I have no margin. I’m the victim! How much are Taylor Swift tickets? Sweet, I’m in. I’ll figure it out, but I’m not missing the show!”

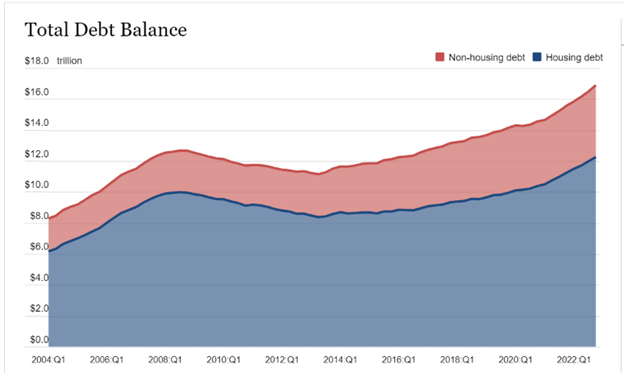

I’m not so sure this example is that extreme. The hard data would corroborate my rant. According to the New York Fed, “mortgage balances shown on consumer credit reports increased by $254 billion during the fourth quarter of 2022 and stood at $11.92 trillion at the end of December, marking a nearly $1 trillion increase in mortgage balances during 2022. Balances on home equity lines of credit (HELOC) increased by $14 billion, the third consecutive quarterly increase and the largest increase seen in more than a decade; the outstanding HELOC balance stands at $336 billion.

“Credit card balances saw a $61 billion increase in the fourth quarter, surpassing the pre-pandemic high of $927 billion. Credit card balances now stand at $986 billion, after declining to $770 billion in 2021Q1. Auto loan balances increased by $28 billion in the fourth quarter to $1.55 trillion, continuing the upward trajectory that has been in place since 2011. Other balances, which include retail cards and other consumer loans, increased by $16 billion. Student loan balances now stand at $1.60 trillion, up by $21 billion from the previous quarter. In total, non-housing balances grew by $126 billion. The share of all current debt transitioning into delinquency increased for nearly all debt types.”

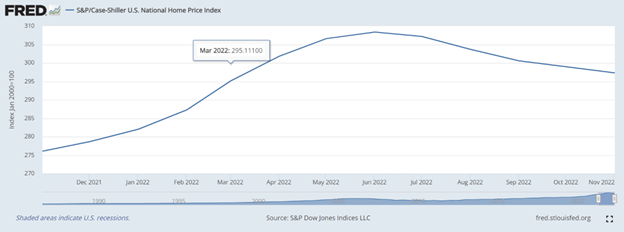

The bulls would contend that air is coming out of the housing bubble, and the spike in household debt is unfortunate for those hard-working people on fixed wages and salaries, but it is also the fault of people not living within their means. As long as the 1% of Americans that own 53% of all stocks are in good shape, then the market is in good shape. Roughly 150 million people, or 55%, of all Americans own stocks in some form or another, but the top 1% have the full attention of market forces.

So, investors shouldn’t lose focus as to why the market trades as well as it does in the face of inflationary pressure. The top 1% can handle 4-5% inflation just fine. They have the financial horsepower to cope with rising prices and the costs of doing business. Anyone over the age of 60 can easily recall the days of the mid-1980s, when many were buying their first home and mortgages dipped below 10% for the first time in a while. At the time, it was celebrated like having hit the lottery. Today’s rate of 7.4% is being treated as an OMG moment because most new home buyers have been living in a perma-stimulus, quantitative easing (QE) bubble for the past 15 years.

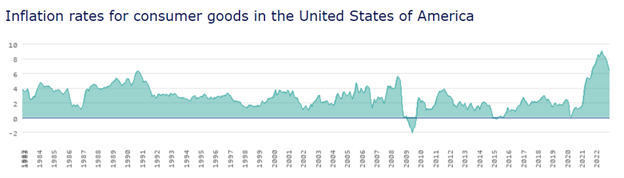

News flash — 4% inflation is historically normal. During the observation period from 1960 to 2021, the average inflation rate was 3.8% per year. Overall, the price increase was 829.57%. An item that cost $100 in 1960 cost $929.57 at the beginning of 2022. For January 2023, the year-over-year inflation rate was 6.4%. One could argue a lot has happened in the past 50 years during which this metric is drawn from. And the stock market has managed just fine in a 4% world. Jobs are plentiful, prices for goods produced allow for decent profits, household wealth increases, real estate appreciates and America generally prospers.

Source: www.worlddatainfo.com

The vocal and divided debate as to whether the economy, S&P earnings, the health of the consumer and the stock market’s price to earnings (PE) valuation will continue to rage on for the days and weeks ahead, because there is simply no consensus. This will continue to foster ongoing volatility until the forthcoming data begins to shed light on economic conditions and whether the eight rate hikes, and the likely two more to come, are priced in. Right now, it is a very hard task to forecast the future, but if one has good stocks, then sitting tight is probably the best plan of action. Sometimes it just pays to show patience.

Sincerely,

Bryan Perry

Editor, Cash Machine

Editor, Premium Income PRO

Editor, Quick Income Trader

Editor, Breakout Options Alert

Editor, Micro-Cap Stock Trader