Tougher Talk on Tariffs Risks Fueling Market Volatility

Investors are doing their best to focus on record second-quarter earnings while letting the war on trade play itself out in the financial media.

It is tough when Microsoft reports five-star results and has almost no impact on the well-being of the broader tech sector. There is a general feeling of broad support for bringing China and other nations in line to fairer trade relationships, but it is becoming clear that this situation could play out over several months, even though the market and investors much prefer a quick fix.

Apparently, China’s President Xi Jinping has no interest in talking fair trade with the United States anytime soon. Per the latest reports on the tit-for-tat tariff dispute, U.S. and China trade officials have taken a pause on further negotiations, having hit an impasse. The Chinese central bank is manipulating the yuan lower to make its goods more attractive to other countries for export and to fatten profits for exporting companies, while the U.S. Dollar Index (DXY) powers higher to a new 52-week high of 95.65 against the yuan and other major currencies.

Fed Chairman Jerome Powell gave a pretty upbeat report on the economy to Congress this week that is contributing to the dollar’s strength, while pressuring crude oil, copper, gold and other commodities. White House Chief Economic Advisor Larry Kudlow stated in an interview at this week’s Delivering Alpha Conference that while some low-ranking Chinese officials were prepared to reach a deal, President Xi was refusing to compromise over Beijing’s trade policies.

“I don’t think President Xi at the moment has any intention of following through on the discussion we made, and I think the president is so dissatisfied with China on these so-called talks that he is keeping the pressure on — and I support that,” Kudlow said.

President Trump recently has threatened to impose a new round of charges on $200 billion of Chinese products, unless the People’s Republic agrees to change its intellectual property practices and high-technology industrial subsidy plans.

The Trump administration released a new list of tariffs on $200 billion of Chinese goods on July 10, as the president continues to broaden the scope of the trade war with Beijing. Trump’s new tariffs will not go into effect immediately but will undergo a two-month review process, with hearings Aug. 20-23. The list comes after warnings by Trump that he may implement tariffs on at least $500 billion, which is essentially most, if not all, Chinese-made goods imported to the United States.

Even though a trade war could culminate in new tariffs imposed by the United States on $700 billion in imported goods globally, it pales in comparison to the $80 trillion global economy. Those tariffs are not even affecting 1.0% of total global commerce, though they could cause ripples and disruptions within the global supply chain, which is the larger risk to the stock market. News of regional manufacturing slowdowns because of supply shortages and bottlenecks will be a negative for investor sentiment.

Against this backdrop of a loud bark of trade rhetoric versus a small bite out of global growth, it shouldn’t make for a big negative on gross domestic product (GDP). But the noise level could get to a place where market volatility spikes in the next couple of months leading up to the September deadline when the $200 billion in additional tariffs on China would commence.

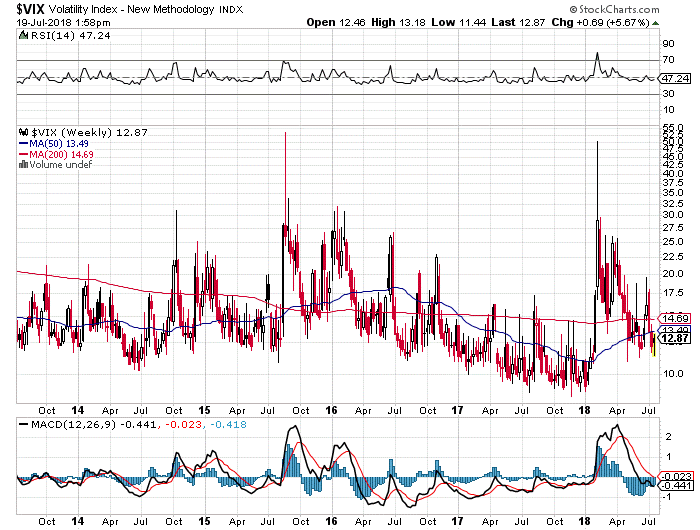

Looking at the CBOE Volatility Index (VIX), which is the most widely followed measure of short-term market volatility, one could argue from a technical standpoint that this index is ripe for a big spike higher. The five-year chart below of the VIX shows the index soaring from 10 to 50 in the first week of this past February triggered by none other than widespread fear of a sudden slowdown in China’s economy.

Since then, the VIX has tested the 12 level twice, putting in a double-bottom formation off of a weekly higher-low formation that is a strong set-up for a sharp move up in the days and weeks ahead. The risk/reward proposition for getting long volatility in the form of either VXX shares or VIX call options is compelling. Once the so-called FAANG stocks of Facebook (Nasdaq:FB), Amazon (Nasdaq:AMZN), Apple (Nasdaq:AAPL), Netflix (Nasdaq:NFLX) and Google/Alphabet (Nasdaq:GOOG), as well as other market favorites, report their second-quarter results in the next week or two, there likely will be a void of significant catalysts to rally stocks.

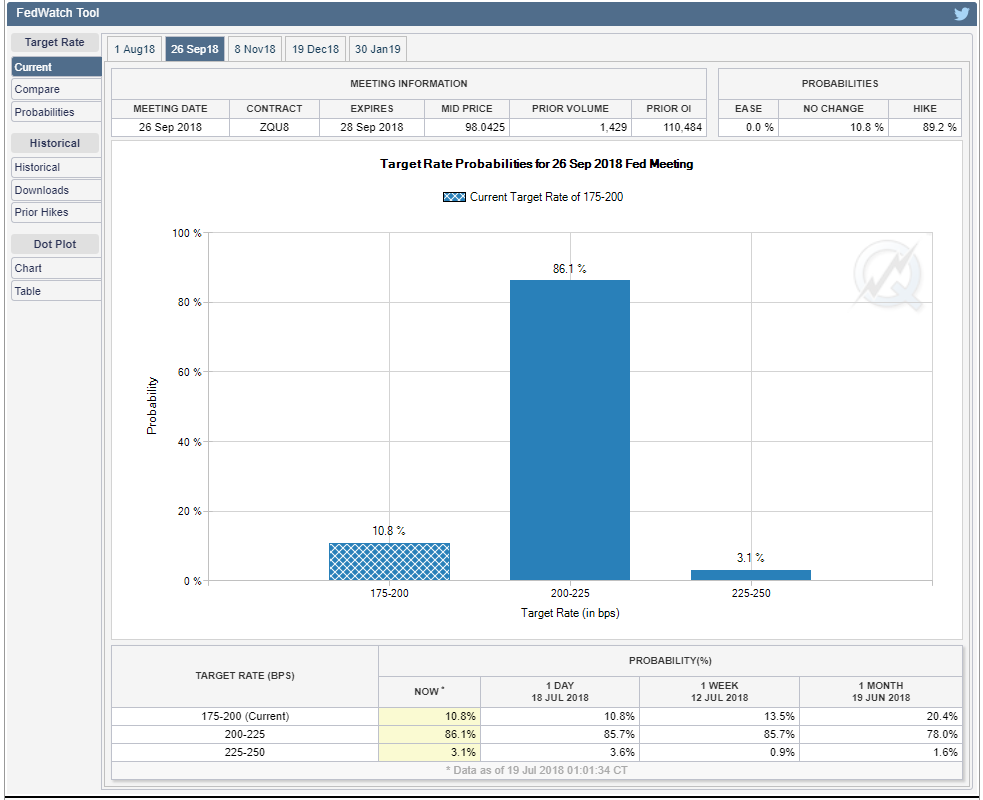

Investors will be contending with the implementation of the next round of tariffs in the first week of September, followed by the Federal Open Market Committee (FOMC) meeting scheduled for Sept. 25-26 where bond traders are predicting an 86.1% probability that the Fed will raise the Fed Funds Rate to 2.00-2.25% (see chart). Short-term inflation data is there to support the next rate hike and that may cause the yield curve to flatten even further, threatening to invert.

U.S. inflation has consumer price inflation near 2.4%, enough to pull Personal Consumption Expenditures inflation, the Fed’s preferred gauge, near its 2% target. This gives me confidence that the central bank will likely forge ahead with raising rates. I do not see inflation sailing far above 2%, but the risk of investor anxiety rising on inflation is there after years of deflation fears dominating. However, while the pick up in U.S. inflation is keeping the Federal Reserve on track to raise rates, it is not high or sticky enough to reverse monetary easing in the euro zone or Japan, which will keep downward pressure on long-term rates.

The other factor that investors have to consider is seasonality. The months of August and September are notoriously weak for equity markets, and this year is setting up to follow that pattern. While a spike in volatility might not repeat the scale of what took place in February, there is a good case for getting long in some volatility in late July.

To put it simply, the low-volatility environment has felt its first tremors of change in 2018. February’s spike in equity market volatility served as the first warning sign. The low volatility of 2017 was abnormal, even in the context of low-volatility periods we have seen since 1980. Steady, above-trend global growth is supportive of further low-volatility regimes, which in the past have tended to play out over many quarters. Yet I do see the potential for greater macroeconomic uncertainty with China’s economy, European credit, oil prices and currency volatility.

So, while I expect the current low-volatility landscape to persist over time, I see potential for episodic spikes amid rising risks which could occur as soon as the next month. I highly encourage all readers of this column to have a portfolio hedging plan in place by the end of July. To follow how I intend to trade volatility in the month ahead in my Quick Income Trader advisory service, click here and take a tour of how weekly and monthly income is generated from market volatility.

It is one thing to be fearful of market volatility and another to have an attitude and a proven approach to profit richly from it. Volatility? Bring it on!