Whipsaw Bond Market Signals a Buy for REITs

Every so often, market volatility spikes, which invariably causes great upheaval in various sectors of the equity and bond markets. Lately, while the stock market has generally behaved itself, the bond market has endured one of the wildest periods of extreme price movement recorded in many years. Because the global bond market now exceeds $100 trillion in size compared to the roughly $65 trillion for the global stock market, there tend to be more muted price movements just due to sheer size and the ability of central banks to intervene to stabilize market conditions.

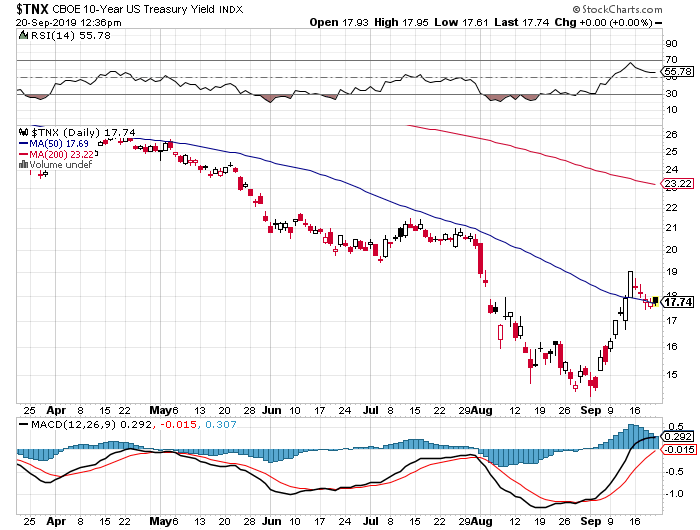

At the end of August and into the first week of September, the yield on the 10-year Treasury traded between 1.45% and 1.50%, down from 2.55% back in early May. A full point drop in the benchmark bond over a three-month period is dramatic. The most likely explanations are the economy fast tracking towards a recession or the collapse of global yields in developed sovereign countries sparking a massive flood of capital into the U.S. Treasury market to lock in rates that were substantially higher.

From the most recent economic data that have crossed the tape in the past two weeks, it is clear the latter scenario is the impetus for the dramatic rally in the bond market. Retail sales, consumer sentiment, business inventories, core inflation, factory orders, the ISM Non-Manufacturing Index, average hourly earnings and private business hires all came in above forecast. It was a parade of upbeat data points that ran counter to and disproved the base case for bearish sentiment that ruled the month of August.

When it became crystal clear to the bond market that the domestic economy was on good footing and news of trade talks being restarted in October was reported, a sharp sell-off in the Treasury market ensued right after Labor Day. As of last Friday’s close, the 10-year T-Note yield had risen to 1.90%.

The narrative about where U.S. bond yields are headed has taken a stunning change of course in just the past week. There was widespread consensus that U.S. bond yields were headed to zero, and for a time that seemed all but certain, until a stunning sell-off crushed the stampede of late-August bond buyers.

Even as the European Central Bank lowered its deposit rate to -0.5% and re-launched its quantitative easing bond buying program to the tune of $20 billion per month in euro-denominated bonds, the mad rush out of U.S. bonds continued. Additionally, the Fed cut the Fed Funds Rate this week by a quarter point to 2.00%.

The rotation out of bonds and bond proxy sectors was also highly evident. Where real estate investment trusts (REITs), utilities, consumer staples and assorted high-dividend stocks and ETFs were delivering very steady returns year to date for income investors, as a group, they have been subject to widespread selling pressure since the beginning of the month. The hardest hit of these assets has been the high-growth REITs within the logistics, self-storage, data center, industrial cannabis greenhouses and cell tower sub-categories.

Just as when it seemed the REIT train had fully left the station, income investors have been given what is, in my view, a truly attractive entry point for initiating and adding to positions in the leading growth REITs. Specifically, shares of cannabis greenhouse operator Innovative Industrial Properties (IIPR) have corrected from $139 to $91. Cell tower and 5G pure-play operator American Tower REIT (AMT) has corrected from $242 to $215.

It’s also my view that the current correction in the secular bond market rally is just that, a correction, and not the beginning of a bear market. Bond prices rallied way too high and way too fast this past month to not undergo a radical bout of consolidation on the heels of better-than-expected U.S. economic data, fresh trade talks and Fed easing.

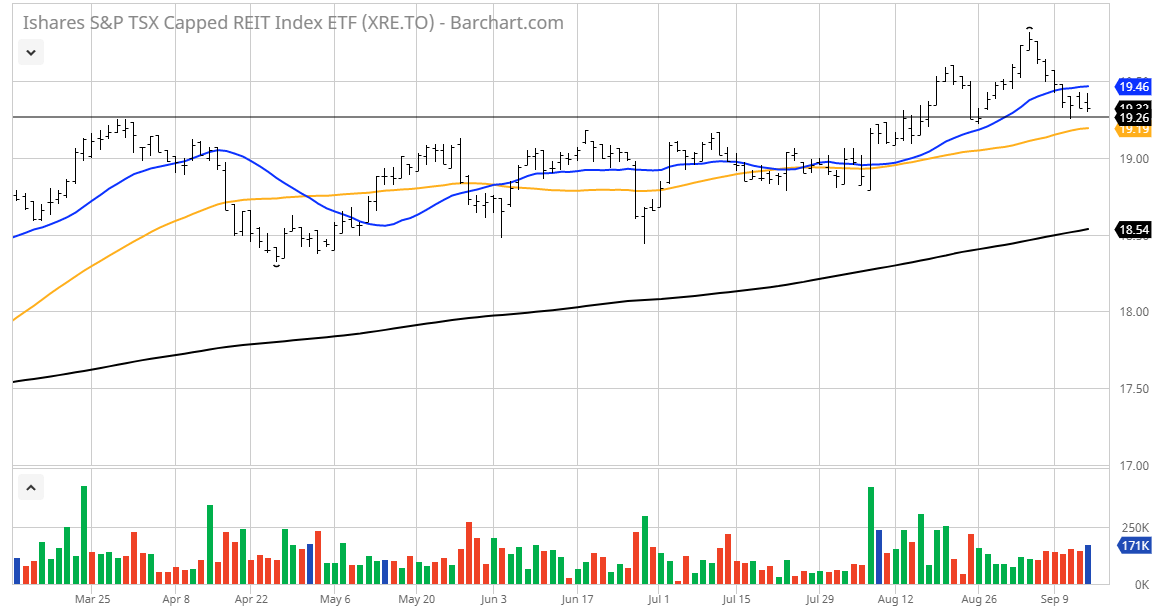

In what is another bullish opportunity within the REIT space, the chart below is that of the Canadian REIT sector in the form of iShares S&P TSX Capped REIT Index ETF (XRE). For all those that admire and respect technical analysis, shares of XRE broke out of a five-month base in late August that coincided with the 10-year T-Note trading with a 1.45% handle.

As the 10-year yield rose back up to 1.90%, shares of XRE have pulled back to key support where buyers should emerge by the month’s end. By the way, shares of XRE sport a 4.20% dividend yield and pay out dividends on a monthly basis.

This falls into the “keep it simple, stupid” category for retirees or anyone else looking to own a real estate portfolio with pristine balance sheets paying 2.2x the yield of the 10-year T-Note and 2.3x that of the SPDR S&P 500 ETF (SPY) while posting a year-to-date return of 15.6%, not including dividends. And all with the simplicity of a click of a mouse.

From the many domestic and international investment scenarios that are colliding for space within the various distribution channels of financial news, opinion and information, this back-and-filling situation in the REIT space is what jumped out most to me. Against the current investing landscape where wild sector rotation, Fed policy, trade talks, Brexit and election politics are dominating the financial media, income investors have what I believe is a unique opportunity in the crème de la crème real estate market to “buy the dip.”