Dividend Investing Weekly

As reported in Barron’s February 2007 issue, “Financial advisor Bryan Perry’s passion is double-digit income investing.”

That same passion for high-yield stocks is what led Bryan to create his Cash Machine service, his book — The 25% Cash Machine, and now his latest project… Dividend Investing Weekly.

Bryan’s new weekly e-letter combines decades-long expertise in income investing with a simple, easy-to-read format that investors of all stripes can put to work for their portfolios.

Current Article

Rising Commodity Inflation Will Pressure Fed to Keep Rate Cuts on Hold

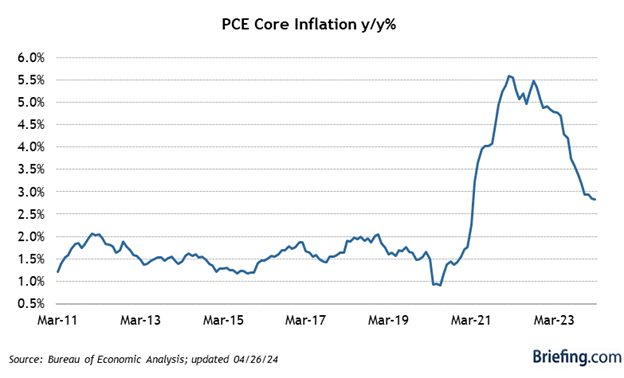

Last year’s fourth-quarter downtrend for inflation looks to have bottomed out at just under the 3% level, at least for the time being. Super sticky components of shelter and services are not showing signs of softening anytime soon, and professional services also continue to remain elevated, especially medical, insurance and education.

Both the PCE Price Index and the Core PCE Price Index, which excludes food and energy, were up 0.3% month over month, which was spot-on with consensus estimates, but they do matter greatly to most consumers. Both energy and food prices are pushing higher during April, led by a doubling in price for cocoa.

There are also renewed price increases for other commodities such as copper, when it was thought that the electric vehicle (EV) boom had hit pause and 18 months of sequentially higher interest rate hikes by central banks would slow construction of residential and commercial projects. Copper is considered the global proxy for economic health. As it stands, copper prices are breaking out to the upside, which is the result of supply constraints and growing demand as the world transitions toward cleaner energy.

Both Citigroup and Bank of America are predicting that copper has entered a new secular bull market where prices will average $10,000 per ton this year and climb to $12,000 per ton by 2026. As countries continue to recover from the pandemic, copper is seeing accelerating demand as recession was all the talk coming into 2024. Wall Street’s newfound bullish stance on copper is also contributing to the recent uptrend that has caught most investors flatfooted. Just recently, Copper surged toward $4.6 per pound and briefly broke the threshold of $10,000 per ton for the first time in two years in London.

Source: www.tradingeconomics.com

Rising oil and copper prices are not the only commodities moving up. Most commodities have charts showing prices trending up and to the right. The CRB Index increased 44.57 points, or 14.79%, since the beginning of 2024, according to trading on a contract for difference (CFD) that tracks the benchmark market for this commodity. Historically, the CRB Commodity Index reached an all-time high of 470.17 in July of 2008. Again, coming into the year, it was widely thought that a protracted slowdown in China and Europe, the second and third largest economies in the world, would keep a lid on commodity prices, but nothing could be further from that forecast.

Source: www.tradingeconomics.com

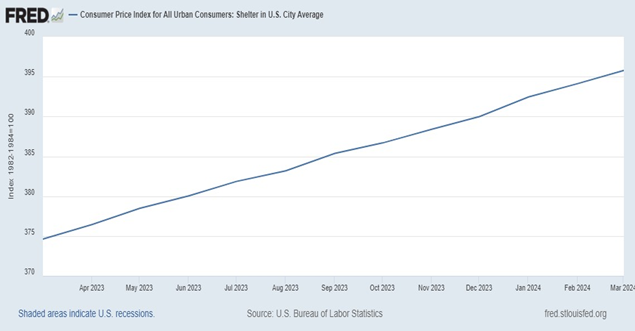

Lastly, the housing shortage in the United States just seems to never keep up with demand, for both new homes and rents. The shelter component accounts for one-third of the total expenditures on goods and services in the Consumer Price Index (CPI) basket. It is the largest expenditure category within the CPI, reflecting costs associated with housing, including owners’ equivalent rent of residences and rent of primary residence.

Here, too, the chart of the shelter index is in a 45-degree angle to the upside and shows no sign of tapering, reflecting a tight supply and near full employment that supports the rising cost of shelter. Until there is some softening of food, energy, hard commodities, services and housing, the Fed’s base case for 2% inflation looks fanciful at best with a clear possibility of there being no rate cuts in store for 2024.

Currently, the price trends are not their friends, as the economy is growing despite 11 rate hikes and sticky price increases. There is an old saying that the cure for higher prices is… higher prices. To be sure, if these trends continue there will be an inflection point where spending does slow, but that time is further out given the upward guidance by home builders and domestic automakers.

Fortunately, it seems the stock market is resetting expectations for the outlook for rate cuts and embracing growth as an equally important catalyst for the bull market to continue marching on.