Fed’s Terminal Rate Looks to Be 5.0%

The latest catch phrase coming from the broad scope of Fedspeak is the terminal rate, known as the level at which the Fed is expected to stop raising interest rates.

With Wednesday’s hike, the fed funds target rate range is now 3.75% to 4%. Stocks rallied sharply late Friday after investors heard some commentary from Boston Fed President Collins, a Federal Open Market Committee (FOMC) voting member, saying that she supports smaller rate hikes going forward, followed by holding the fed funds rate range at a restrictive level.

In addition, Chicago Fed President Evans, a non-voting member, agreed that it makes sense to shift to smaller rate hikes. On a related note, JPMorgan expects a 50-bps rate hike in December, followed by a 25-bps hike in February.

The latest CME FedWatch Tool estimate shows a 52% probability for a 50-bps rate hike at the Dec. 14 FOMC meeting and a 48% chance of a fifth 75-bps hike that would take the Fed Funds Rate up to 4.50-4.75%. These numbers will shift radically over the next three weeks as the next batch of economic data crosses the tape.

What it does show, though, is that the Fed acted aggressively right in front of the highly charged midterm elections, in what is a clear message central bank leaders are on high inflation alert, feeling further aggressive action in the form of rate hikes and quantitative tightening to the tune of $95 billion per month is essential to breaking inflation. Since the market is a forward-discounting mechanism with quite possibly the terminal rate reaching 5.00-5.25%, it is probably a good time to start considering some fixed income assets and bond equivalents, even if the terminal rate stays at an elevated level for several months.

The same problems that ignited inflation are pretty much still in place — increases in wages, salaries, food, energy, rents and professional services. The cost to travel is extremely high and there remain key supply chain bottlenecks that contribute to the cost of certain goods on the rise.

Assuming inflation does see some pressure relieved in the months ahead where the overall rate comes down to the 5-6% range, the bond market will be basically meeting inflation where it is at, representing a sense of equilibrium that should be constructive for equities and certainly an opportunity for income investors to lock in some juicy rates that are consistent with the rate of inflation.

Depending on one’s view of whether the U.S. economy will experience a soft or hard landing, for the first time in a long while, government bond yields and other fixed-income assets have offered investors rates that could make them stop and think about putting their cash to work in risk assets.

The the 2/10 Treasury spread is at roughly 50 bps, implying a material slowdown in gross domestic product (GDP) during 2023. With any whiff of receding inflation, this spread will narrow sharply with the yield curve flattening and hopefully followed by normalization where long-term rates are higher by 30-50 bps over short-term rates.

But a lot of constructive data must occur before this transition can take place. This window of a terminal rate scenario has severely punished Treasuries, corporate bonds, municipal bonds, convertible bonds, preferred stocks, real estate investment trusts (REITs) and utilities may close sooner than expected, if the market decides peak inflation and peak rates are a product of Q1 2023.

Taking into account a few exchange-traded funds (ETFs) and closed-end funds that trade at huge discounts to Net Asset Value (NAV), I would contend that the time is now to lock in some yields, with the understanding that the cycle of rate hikes is nearing completion. If so, then a couple examples of what investors can look at for yield are:

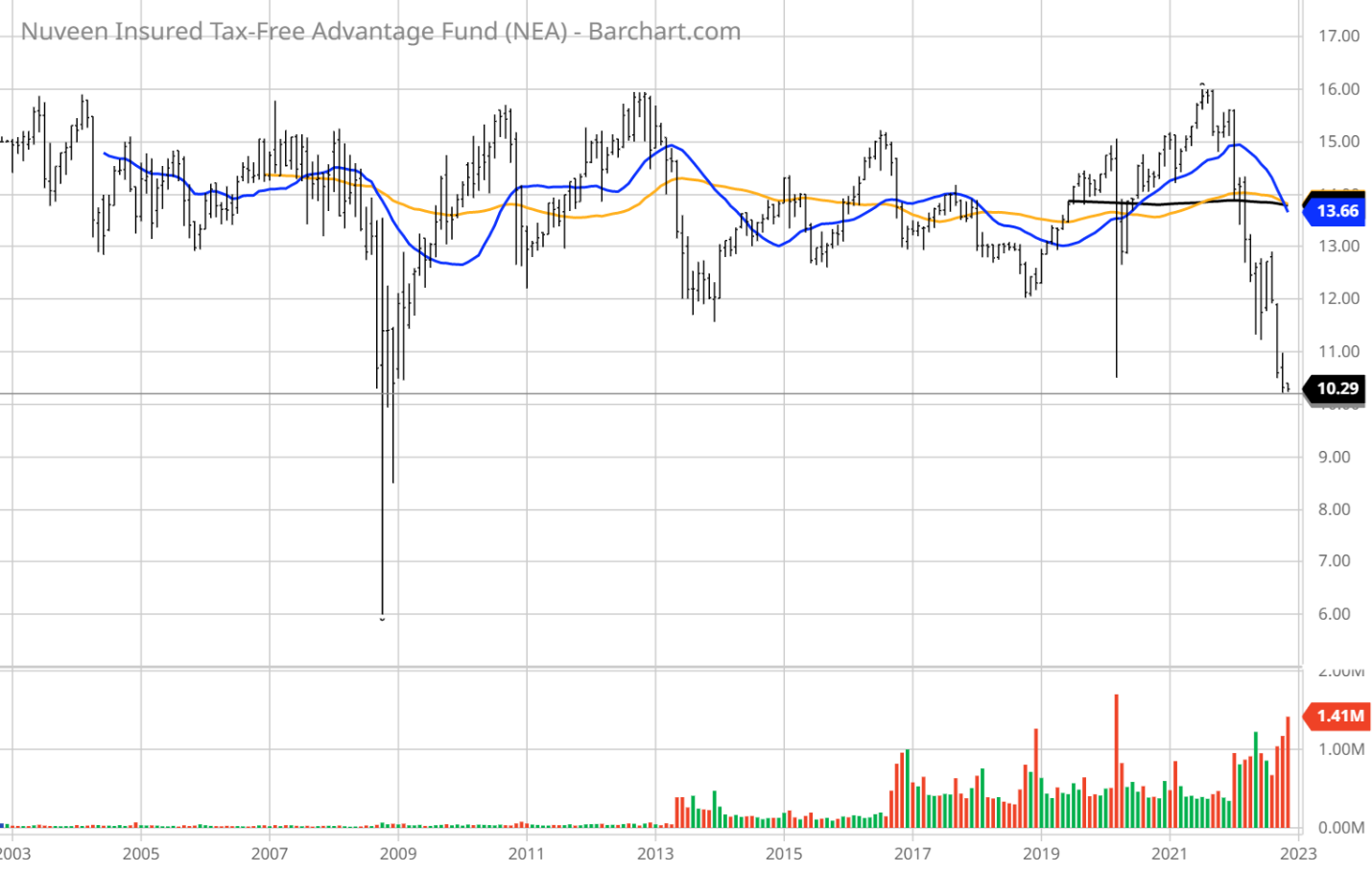

Nuveen AMT-Free Quality Municipal Fund (NEA), a national portfolio trading at an 11.9% discount to net asset value (NAV), sporting a 5.2% distribution yield that pays monthly, with just over 90% of the holdings being investment grade. This fund uses leverage to boast such an attractive yield.

Shares of NEA are trading 35% below their high. Add in the nearly 12% discount to NAV and we’re talking a 45% correction from peak to what may be the trough. For the income earners in the highest tax bracket, the yield has a taxable equivalent rate of over 10%.

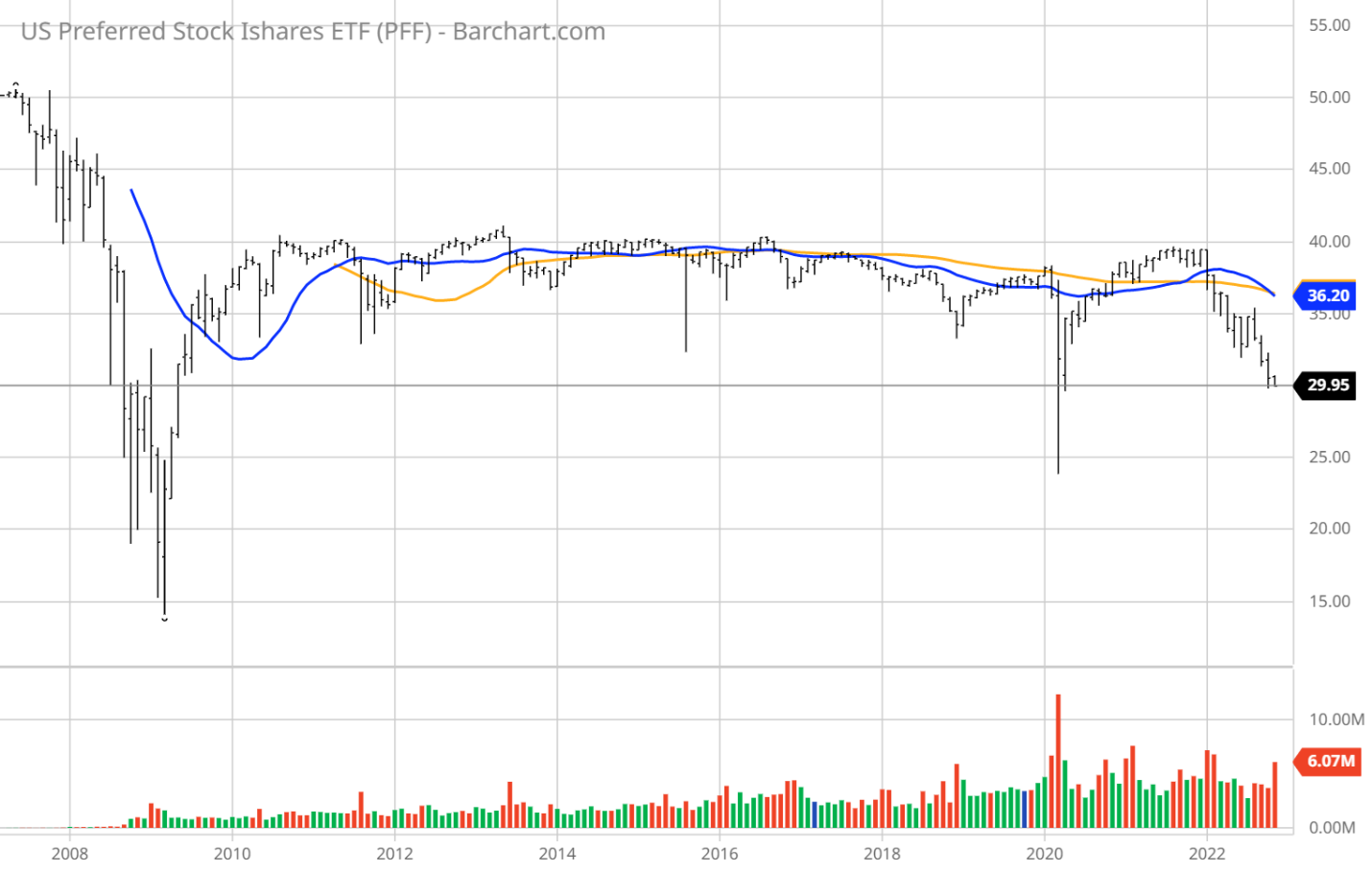

For retirement accounts, or investors who want something outside the municipal market, the iShares Preferred & Income Securities ETF (PFF) is paying out a current yield of 5.6% and trading 24% below its multi-year high and paying dividend monthly.

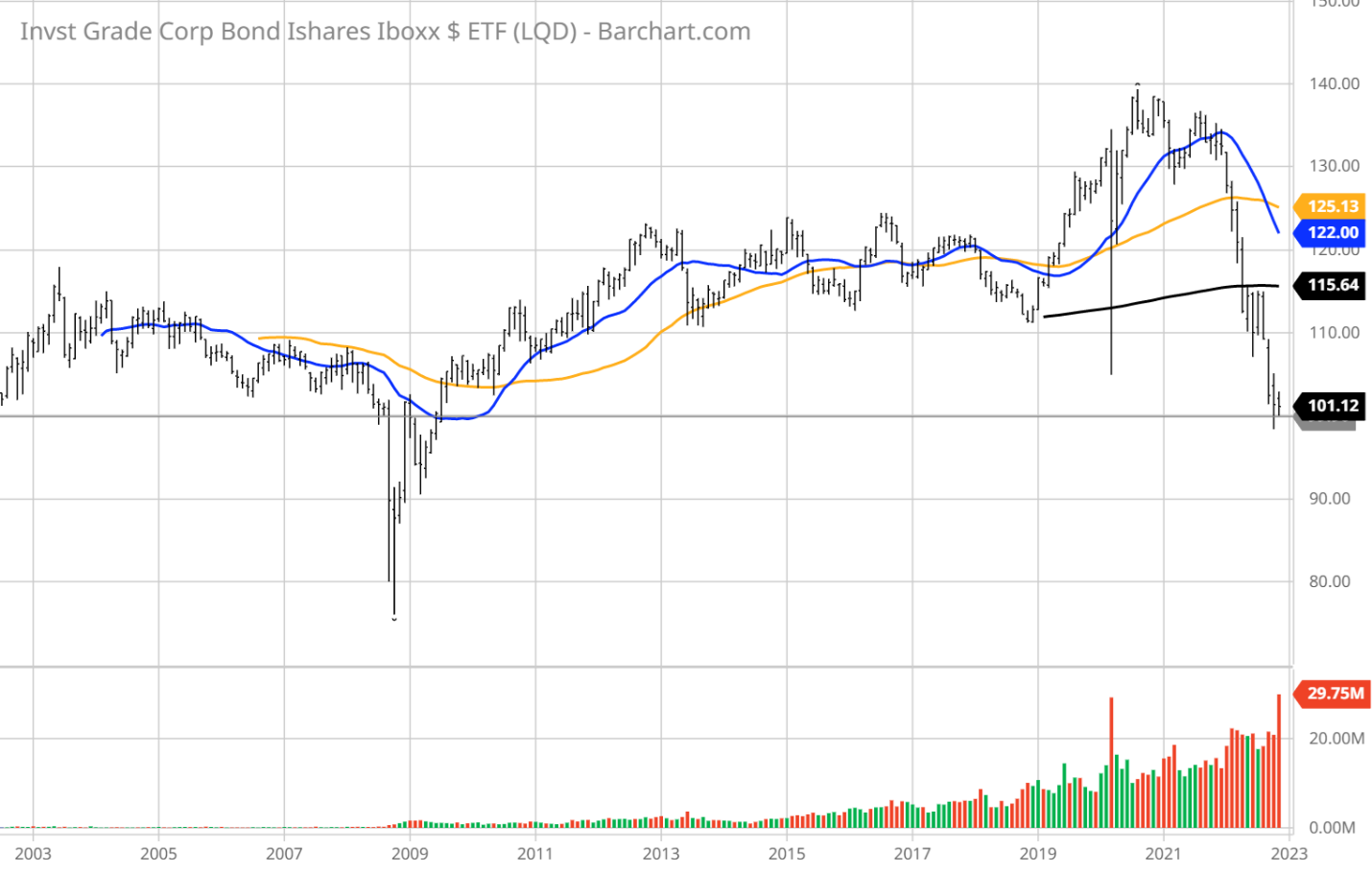

And for a pure play on the investment-grade corporate market, the iShares Investment Grade Corporate Bond ETF (LQD), sports a 5.8% distribution yield, average yield to maturity of 5.95%, average weighted maturity of 13.5 years, and a portfolio effective duration of 8.2 years. After peaking in 2020 at $140, shares of LQD are currently trading at $101, 27% below that high.

If for whatever reason or circumstances the Fed does in fact pivot in the next year to lower rates, these three assets and many others of similar nature will be big winners. For those savvy enough to shop for individual bonds, preferreds, converts and Treasuries, constructing a custom portfolio reduces the risk of ETF funds having to buy bonds with lower yields as prices are rising when capital flows surge back into these asset classes. Just screen for the top holdings of each and build your own portfolio that isn’t traded or compromised by outside fund flows.

It is a feat of timing to call for a terminal rate for fed funds or a bottom in bond prices, but the time is upon income investors to be thinking about allocating capital back into fixed income if the forward data prove to support the case for peak inflation.