Record Dividends and Buybacks Provide Market with Silver Lining

For five weeks, the S&P has slid lower amid trade tensions with China, while the European Union (EU) has continued to devolve into a body that is rapidly losing support as populist and nationalist movements have taken hold throughout Europe.

The resignation of British Prime Minister Theresa May brought more uncertainty to the Brexit process and triggered a nasty sell-off in the pound. And new pending tariffs on Mexican imports are putting further downside pressure on the stock market.

Both China and the EU are situational challenges. The U.S. stock market had become a safe haven for investors as it has been supported by a healthy labor market, bond yields hitting multi-year lows, vigilant corporate stock buybacks and low inflation in most of the areas that impact businesses and consumers alike. But the market has narrowed in recent weeks. It was reported on CNBC that 56% of S&P 500 stocks are in a bear market, so stock selection is at a premium as the S&P currently is trading at roughly the same level it had at this time a year ago.

I hope that at the G20 meeting on June 28-29 in Osaka, Japan, President Trump and President Xi can produce some new progress on trade. But that possibility is a full month out.

And now, it seems that the United States is getting closer to an armed conflict with Iran. As many of us are aware, National Security Advisor John Bolton, working with Secretary of State Mike Pompeo, have begun telling the population starting with the President about alleged intelligence reports that came into their possession from Israel. These reports say that there would be imminent attacks from Iranian forces or Iranian supported factions in Iraq against U.S. forces.

I sense no public support for an avoidable war in the Middle East. Thus, I believe President Trump will not commit to one in front of an election year. Rather, he will make every effort to just get out of the region — despite pressure from the military industrial complex. Our vital interest in the region was oil and now its not.

Israel has excellent intelligence and precision strike capability. If there is clear-cut evidence of Iran making weapons-grade uranium, those targets can be taken out by Israeli air strikes. Oil prices actually fell hard in the past two weeks, amidst the saber rattling, on much higher weekly inventory data. WTI closed the week at $55/bbl. Oil traders are betting that war with Iran is not on the table.

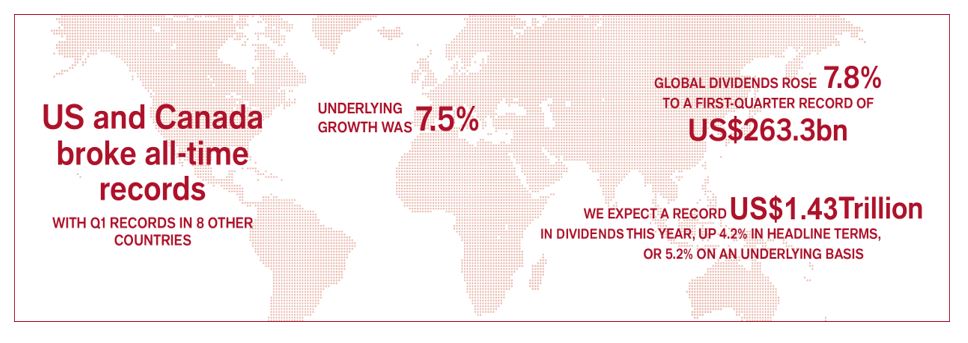

On a much more positive note, global dividends reached a first-quarter record of $263.3 billion, rising 7.8% despite investor anxiety about a slowing world economy. The Janus Henderson Global Dividend Index showed that U.S. dividends rose 8.3% to reach a record $122.5 billion for the quarter.

The report also stated that, “Almost 90% of the companies featured within the index raised dividends, the highest increases coming from the banking sector.” Janus Henderson added that, “Investors can look forward to dividend growth of around 4% to 5% in 2019 and another record year for dividend payments.”

Source: Janus Henderson

The report cited the Asia-Pacific region as posting the strongest year-over-year headline growth of 14.7% and exceeding the global average for the past five years. This is because Japan has begun to adopt a more pro-dividend culture with its aging population.

Stock buybacks for the first quarter of 2019 also are on pace to set yet another record. According to Michael Schoonover, chief operating officer of Catalyst Funds, as of March 15, companies had already bought $253 billion worth of their own stock. This is $18 billion more than for the same period a year ago.

A rebounding economy, low interest rates and the windfall from the 2018 tax cuts are driving the record share repurchases and dividend increases that, in spite of what may come of China, Europe, Mexico and Iran, are providing an underlying bid for U.S. dividend-paying stocks. These are huge numbers that will support a new paradigm and a higher market, especially if quarterly sales and earnings continue to surprise to the upside as was the case in the first quarter of 2019. The headlines are full of angst, but the data still very much favors the bulls.