Targeting High-Yield Assets With Inflation on the Rise

Recent data show real GDP growth and core inflation are rising at a faster pace than previously forecast. How both of these “nice problems to have” are addressed by the Fed is one thing, but more importantly, how income-oriented investors should position their portfolios is another.

Signs of inflation have been building for weeks, if not months now. Simply checking out at the grocery store or gas station reveals this clearly. In fact, there are signs of inflationary pressures at work that are no one-month one-offs. Just this past week, investors received a slew of core economic data that build a solid case for further rises in inflation data as well as bond yields rising across the curve.

- Empire State Manufacturing for February was 12.1 versus 7.5 consensus

- Retail Sales for January up 5.3% versus 0.8% consensus

- Retail Sales Ex-Auto up 5.9% versus 0.7% consensus

- Producer Price Index for January up 1.3% versus 0.5%

- Industrial Production for January up 0.9% versus 0.6% consensus

- Capacity Utilization for January at 75.6% versus 74.9% consensus

- Building Permits for January at 1881K versus 1670K consensus

The Five-Year, Five-Year Forward Inflation Breakeven Index measures the expected inflation rate (on average) over the five-year period that begins five years from today. The current Five Year, Five Year inflation expectation rate as of February 19, 2021, is 1.99. As one of the two mandates supported by the Fed, getting the rate of inflation back up to 2% looks to have been achieved, or nearly so.

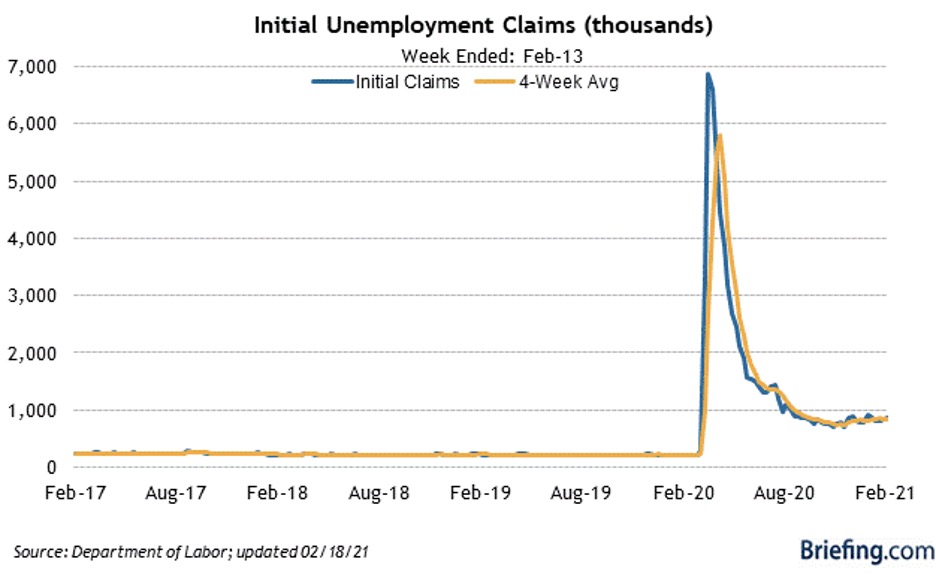

The other mandate of full employment, representing an Unemployment Rate below 5%, is and will be fleeting, it seems, for the foreseeable future. Despite the stimulus packages rendered in their various forms over these past twelve months, the job market for tens of millions of Americans is not improving. Initial Jobless Claims, for the week ending on Feb. 13, increased by 13,000 to 861K versus 775K.

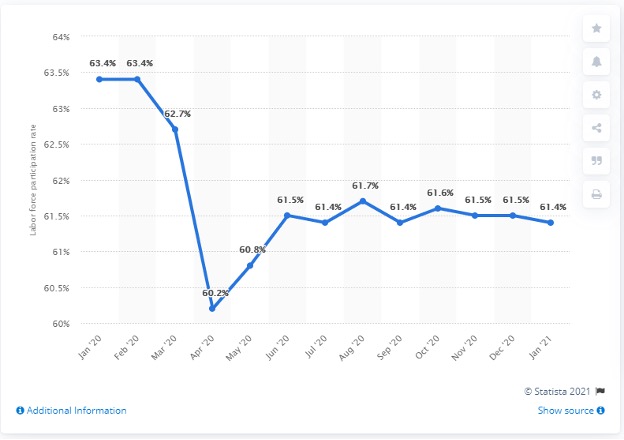

Although the Unemployment Rate fell to 6.3% from 6.7% in January, it was due to the fact that the Labor Participation Rate also fell to 61.4%, virtually unchanged from June of 2020 and down from the prior three-month period. Translated — more Americans who are eligible to work in the everyday U.S. economy have stopped looking for jobs.

Adding to this dilemma is the current push by the Democrat-controlled Congress to mandate a federal $15 per hour minimum wage. This policy should be regionally implemented as scores of small businesses, already dealing with high rents and growing state and city regulations, could be crushed by the $15 per hour minimum.

One-third of small businesses anticipate laying off workers if Congress increases the federal minimum wage to $15 per hour, according to the latest CNBC|SurveyMonkey Small Business Survey. A recent Congressional Budget Office analysis forecasts that a $15 minimum wage would lift 900,000 Americans out of poverty, but result in 1.4 million fewer jobs. It’s a real conundrum that needs to get worked out to the benefit of all.

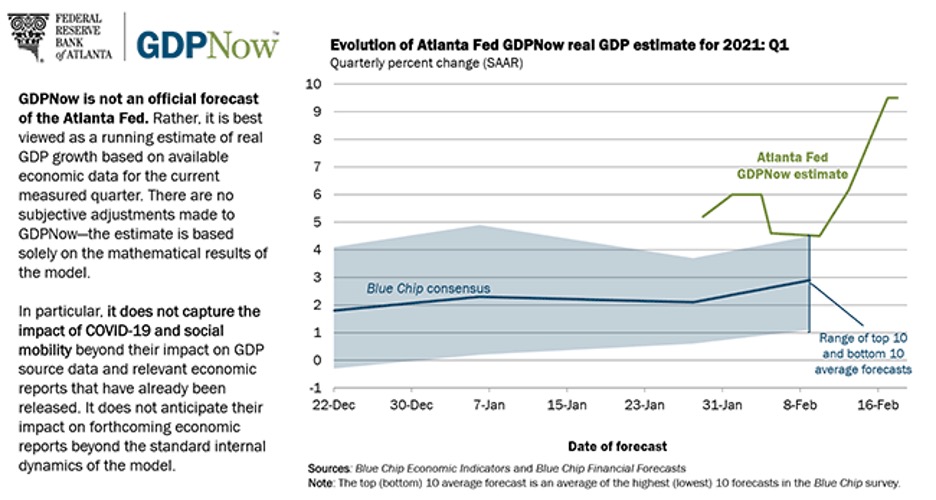

Regardless of the lagging labor market, the general tone of the corporate economy is picking up speed, led by strong growth within the S&P 500 and the largest privately held companies in the United States. The latest read from the Atlanta Federal Reserve GDPNow report estimates GDP growth for the first quarter of 2021 at 9.5%, nearly double the prior estimate.

Companies are producing more goods and services with fewer employees, a natural byproduct of any economic crisis. On the surface, this looks hugely promising for job prospects, and hopefully, it works out that way. But, as so many companies reported within their Q4 earnings transcripts, advances in technology and reduced remote workforces are helping to pad the bottom line.

The tale of two economies will continue to exist until the airline, cruise line, restaurant, lodging, amusement park, custodial, corporate cafeteria and a host of other pandemic-plagued businesses come back to life.

Against this backdrop of rising GDP and higher rates of inflation, money is flowing out of the long end of the bond market. The yield on the benchmark 10-year Treasury Note is up to 1.34%, and in my view, headed right to 1.5%, and possibly higher.

For investors seeking income that benefits from rising bond yields and equities, there are some clear choices. I’ve noted previously that one of my favorite asset classes in this environment is convertible debt, bonds and preferred stocks that can be converted into the underlying equities, thereby benefiting from stock appreciation.

Retail investors can buy closed-end funds that use 20-30% leverage utilizing cheap, short-term rates to generate yields of 5-7% that pay monthly dividends. This is a simple and easy way to buy into this favored asset class.

High-quality business development companies (BDCs) are another class of security to own when the economy is expanding. Most loans made by BDCs to small-to-medium-sized businesses are structured as floating rates.

When rates rise, those loans are adjusted to receive more interest. Those higher income streams are passed on in the form of higher dividends because BDCs are structured like REITs and have to pay out 90% of income as regulated investment companies. The highest-rated BDCs pay out yields of 7-12%.

Closed-end covered-call funds that invest in blue-chip, market-leading stocks are also a fine way to own the best stocks while deriving a 5-8% annual income stream. Some of these funds pay monthly.

And don’t forget select subclasses of REITs that invest in e-commerce logistics and other hot growth sectors of the economy. Here, too, one can find 3-6% dividend yields.

Energy assets tied to oil and gas is the one sector where current yields are juicy, but the future of which holds more risk than I’m willing to endorse at this time.

It takes some due diligence to find the best-of-breed stocks and funds in each of these assets that trade outside the conventional Treasury inflation-protected securities (TIPS) market and other commercial floating-rate instruments that pay under 2%. But after adjusting for rising inflation and taxes, making 2% generates a negative return on an absolute basis going forward.

These latest inflation and GDP readings are a wake-up call to bond investors and income investors alike. It’s a good time to shorten up duration in bond portfolios and consider adding exposure to those assets that benefit from borrowing at or near the Fed Funds Rate and lending long and owning assets tied to stock market performance.