The Road Ahead for Rates Looks Flat for Longer

Looking at the big picture for the stock market going forward, one only needs to pay close attention to the bond market. Rising bond yields will prove to be a bigger challenge to the market’s leading growth companies, a commonly understood assumption by most investors. And though there is strong disagreement as to whether the Fed is justified in taking the Fed Funds Rate up toward 6.0%, the bond market is only placing a 13% chance of a quarter-point hike at the Sept. 20 Federal Open Market Committee (FOMC) meeting.

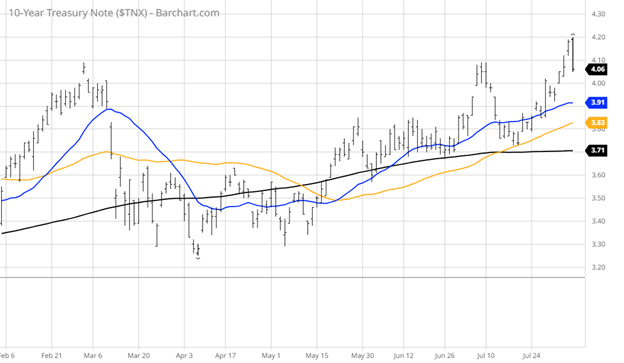

The odds of another rate hike were diminished by last Friday’s July employment report, where non-farm payrolls came in a tad light of forecast coupled with the unemployment rate dropping to 3.5% from 3.6% registered in June. It took the heat off Wednesday’s hot ADP private payrolls report that came in way above estimates. ($324 thousand versus $185 thousand) and helped restore order from a sharp selloff in the Treasury market that sent five-, 10-, 20- and 30-year yields up and through 4.0%. The benchmark 10-year T-Note touched 4.20%, the highest level since November 2022, before settling out the week at 4.06%.

The on again, off again recession narrative can be seen in the price action of the 10-year T-Note that has moved from 3.6% at the end of May to 4.1% this past week, after Fed Chair Jerome Powell said “the central bank’s staff no longer forecasts a U.S. recession, and we do have a shot for inflation to return to target levels without high levels of job losses.”

In the same breath, Powell also said that there was “a lot left to go to see such a soft landing. So, the staff now has a noticeable slowdown in growth starting later this year in the forecast, but given the resilience of the economy recently, they are no longer forecasting a recession.” What these two charts seem to imply is that while rates are normalizing, the Fed will likely pause at the September meeting and possibly raise once more at the November or December meeting if the economy continues to prove resilient.

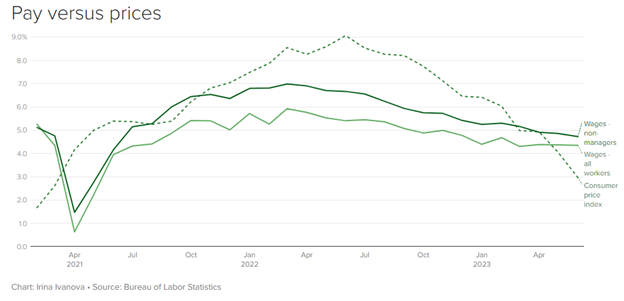

I think one statistic that was reported back on July 18 that was most encouraging, was for the first time in two years, pay is finally rising faster than consumer prices, according to data from the Bureau of Labor Statistics. Average hourly pay has grown at an annual rate of 4.4% for the last three months, topping the Consumer Price Index, which rose at a rate of 3% in June and 4% in May. This is a small win for workers, but also sends a message that tight labor supply and solid wage growth will probably result in the Fed Funds Rate staying at the current 5.25-5.50% level for quite some time.

This assumption does run counter to the wider belief that the Fed will begin cutting rates starting around March 2024. Investors will get July inflation data this week when the Consumer Price Index (CPI) and Producer Price Index (PPI) are released, both of which are forecast to increase by 0.2%. The CRB Index rose by nearly 10% in July, and could disrupt the recent downtrend.

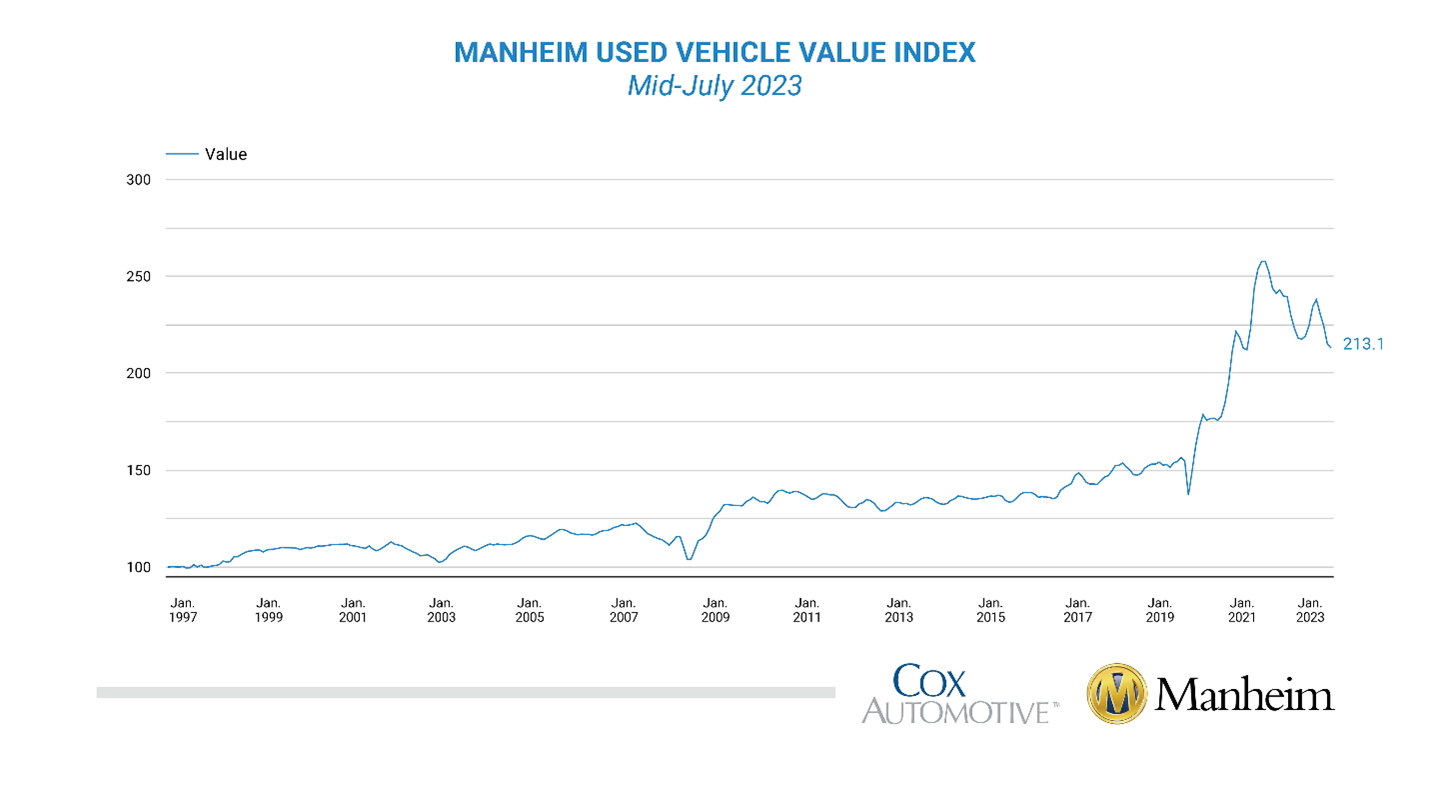

With food and energy prices rising in the past month, a lower inflation reading will likely be the result of a softening in the shelter component and new and used car component. All major used vehicle market segments saw seasonally adjusted prices that were lower year over year in the first half of July.

Rent growth around the country is back at pre-pandemic norms — growing about 1-3% per year, according to real estate data firm CoStar Group. In some recent hot spots, including Austin and Atlanta, prices are actually falling.

“The rental market is finally taking a breath,” said Igor Popov, chief economist at Apartment List. “This summer looks a lot different from the last two summers: We are getting to a more stable period, and in some parts of the country, renters are back in the driver’s seat.”

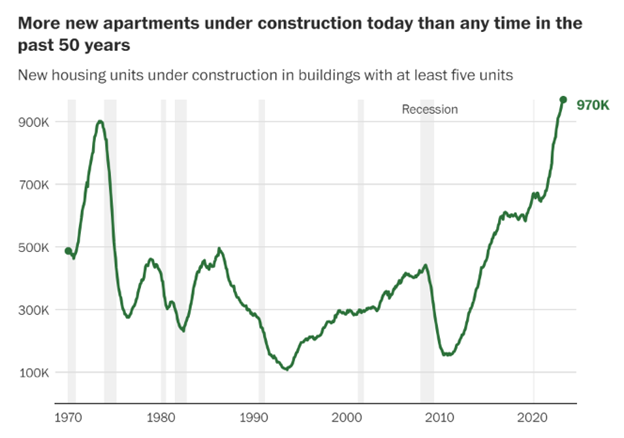

The biggest reason for that slowdown: more housing. Nearly one million new apartment units — an all-time high — are under construction around the country, census data shows. Of those, 520,000 are expected to hit the market this year, with another 460,0000 to follow in 2024, according to CoStar.

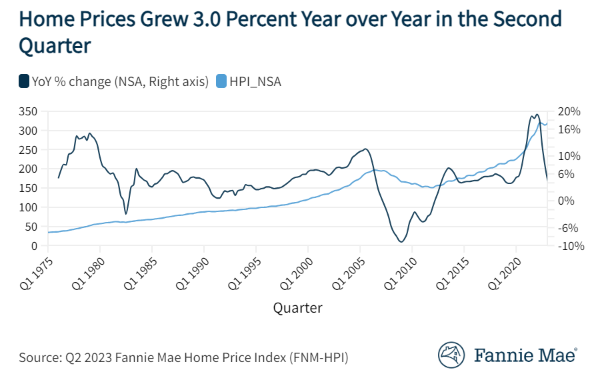

New home prices are holding up even as mortgage rates trend higher due to ongoing supply shortages, but seeing some of the air come out of the rental market is good news. There is some leveling off of price increases for home sales, up only 3.0% year over year. So, here too, housing inflation is moving in the right direction — lower.

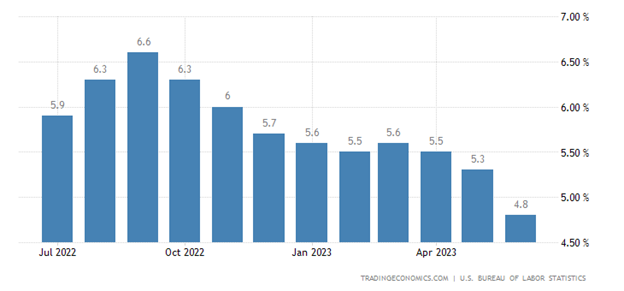

As of June’s reading, the core inflation rate for the U.S. stands at 4.8% and needs to come down further to enable the servicing of the massive U.S. debt that Fitch and other rating agencies see as a long-term threat, citing “failure of the U.S. authorities to meaningfully tackle medium-term fiscal challenges” and a growing debt burden.

Richard Francis, a senior director at Fitch, told Reuters when asked about the timing of the downgrade, that the agency “wanted to kind of really take a deep look” at long-standing concerns around governance and the U.S. debt profile.

“Fitch isn’t telling anybody anything they don’t already know,” said Mark Sobel, a former longtime Treasury official who is now U.S. chairman of financial think-tank OMFIF. Longer term, he said, “neither political party has evinced the guts to begin making the sacrifices needed on both the spending and revenue sides — which will only increase as time marches on.” Even if the Fed doesn’t raise rates any further, the debt continues to soar, because as low-yield existing debt matures, it is replaced with new debt at higher prevailing rates.

To this point, it is pretty imperative the Fed gets rates back down. We need some good numbers because the bond market is acting like a Nervous Nellie, and with this week’s inflation data on deck, investors will know if the recent favorable trend is still their friend.

P.S. Come join our Eagle colleagues on an incredible cruise! We set sail on Dec. 4 for 16 days, embarking on a memorable journey that combines fascinating history, vibrant culture and picturesque scenery. Enjoy seminars on the days we are cruising from one destination to another, as well as dinners with members of the Eagle team. Just some of the places we’ll visit are Mexico, Belize, Panama, Ecuador and more! Click here now for all the details.